Revolutionizing Risk: The Transformative Impact of Artificial Intelligence on Financial Risk Management

Table of Contents

- Introduction: A Paradigm Shift in Financial Risk Management

- The Inadequacies of Traditional Risk Management in a Digital Age

- The Core Engine: Machine Learning in Financial Risk Assessment

- Real-World Implementation: Case Studies and Proven Impact

- Navigating the Future: Trends, Challenges, and the Path Forward

- Conclusion: Towards a More Resilient and Intelligent Financial System

Introduction: A Paradigm Shift in Financial Risk Management

The financial industry is undergoing a profound transformation, driven by the integration of Artificial Intelligence (AI). This evolution is not merely an incremental improvement but a fundamental paradigm shift in financial risk management. For decades, the practice has been anchored in a reactive posture, relying on historical data and established statistical models to manage uncertainty. Today, AI is enabling a transition to a proactive, predictive, and holistic framework capable of navigating the complexities of a hyper-connected global economy. As one academic paper notes, AI has "fundamentally transformed financial risk management, enabling firms to identify, assess, and mitigate risks at unprecedented speed and scale" (SSRN, Apr 2025).

This shift is propelled by a confluence of powerful forces: the exponential growth of "big data," encompassing both structured financial records and unstructured sources like news and social media; monumental advancements in computational power; and the increasing sophistication of machine learning (ML) and deep learning algorithms. Traditional rule-based systems are proving less effective in this dynamic digital landscape, creating an urgent need for more intelligent solutions. According to research from the University of California, AI is projected to be integral to risk management in over 80% of large financial institutions by 2028 (Markovate, Dec 2024), underscoring the rapid pace of this technological adoption.

This paper will explore the multifaceted impact of AI on financial risk management. It begins by examining the inherent limitations of traditional methods to establish a baseline for AI's disruptive role. It then provides a deep dive into the core machine learning technologies driving this change, analyzing their application across key risk domains. Through real-world case studies, the paper will demonstrate the tangible benefits of AI implementation. Finally, it will offer a forward-looking perspective on emerging trends, critical challenges, and the ethical considerations that must be addressed to forge a more resilient and intelligent financial system.

The Inadequacies of Traditional Risk Management in a Digital Age

To fully appreciate the transformative power of AI, it is essential to first understand the limitations of the conventional risk management frameworks that have long dominated the financial industry. These methods, while foundational, were designed for a simpler, slower, and more data-scarce era. In today's fast-paced, digital-first world, their inadequacies have become increasingly apparent.

Reactive Nature

The most significant drawback of traditional models is their fundamentally reactive nature. They are built upon historical data, using tools like Value at Risk (VaR) and regression analysis to extrapolate past trends into future probabilities (NetSuite, Jun 2025). This approach is effective when the future resembles the past, but it falters in the face of unprecedented events or "black swan" scenarios. Traditional models analyze what *has happened*, not what *could happen*, leaving institutions vulnerable to novel threats like flash crashes, systemic contagion from new financial instruments, or sudden geopolitical shocks.

Data Processing Constraints

The modern financial ecosystem generates data at an astonishing volume, velocity, and variety. Traditional systems are ill-equipped to handle this deluge. They primarily process structured data—neatly organized in spreadsheets and databases—but struggle immensely with unstructured data. Critical risk indicators are now often found in unstructured sources such as news articles, regulatory filings, social media sentiment, and even satellite imagery. The inability to analyze this rich, contextual information in real-time creates a significant blind spot, as noted by industry analyses highlighting AI's ability to process these diverse data streams (XenonStack, Apr 2025).

Linearity and Simplistic Assumptions

Many conventional risk models are based on linear assumptions and presume normal distributions of returns and risks. However, modern financial markets are characterized by complex, non-linear relationships and interconnected feedback loops. Traditional models often fail to capture these intricate dynamics, providing an oversimplified view of risk (Finextra, Sep 2024). This can lead to a dangerous underestimation of tail risks and contagion effects, where a small event in one part of the system can trigger a cascade of failures across the market.

Manual Effort and Latency

The operational backbone of traditional risk management relies heavily on manual, labor-intensive processes. Data collection, cleansing, analysis, and reporting are often slow and prone to human error. This latency creates a critical gap between the moment a risk is identified and when mitigation strategies can be implemented. In a world where market conditions can change in milliseconds, this delay is a significant liability. This reactive, manual approach not only increases operational costs but also struggles to keep pace with the accelerating speed of business and regulatory demands (Workday, Apr 2025).

The Core Engine: Machine Learning in Financial Risk Assessment

Machine learning (ML) is the driving force behind AI's revolutionary impact on risk management. It moves beyond the static, rule-based logic of traditional systems to create dynamic models that learn from data, identify complex patterns, and make predictions with increasing accuracy. This section dissects the key ML algorithms and their applications across the spectrum of financial risks.

Foundational ML Models and Their Applications

A variety of ML models are being deployed, each with unique strengths suited to different risk assessment tasks. The choice of algorithm depends on the nature of the data, the complexity of the problem, and the need for interpretability.

- Logistic Regression: Often a starting point for classification tasks, Logistic Regression is used for credit scoring and initial fraud detection. Its primary advantage is interpretability—it's relatively easy to understand which factors influence the outcome. However, it struggles with complex, non-linear relationships in data (Number Analytics, Mar 2025).

- Random Forest & Gradient Boosting (XGBoost, LightGBM): These ensemble methods are industry workhorses. They combine multiple decision trees to achieve high accuracy and are adept at handling large, complex datasets. XGBoost, in particular, is renowned for its performance and efficiency in predicting credit defaults and detecting sophisticated fraud (LinkedIn, Jan 2023). Studies show Gradient Boosting models consistently outperform many other algorithms in accuracy for credit risk prediction (The American Journals, Apr 2025).

- Support Vector Machines (SVM): SVMs are powerful for classification, creating a clear boundary to separate data points. They are effective in credit risk assessment by distinguishing between good and bad borrowers and can identify subtle patterns indicative of fraudulent transactions (BytePlus).

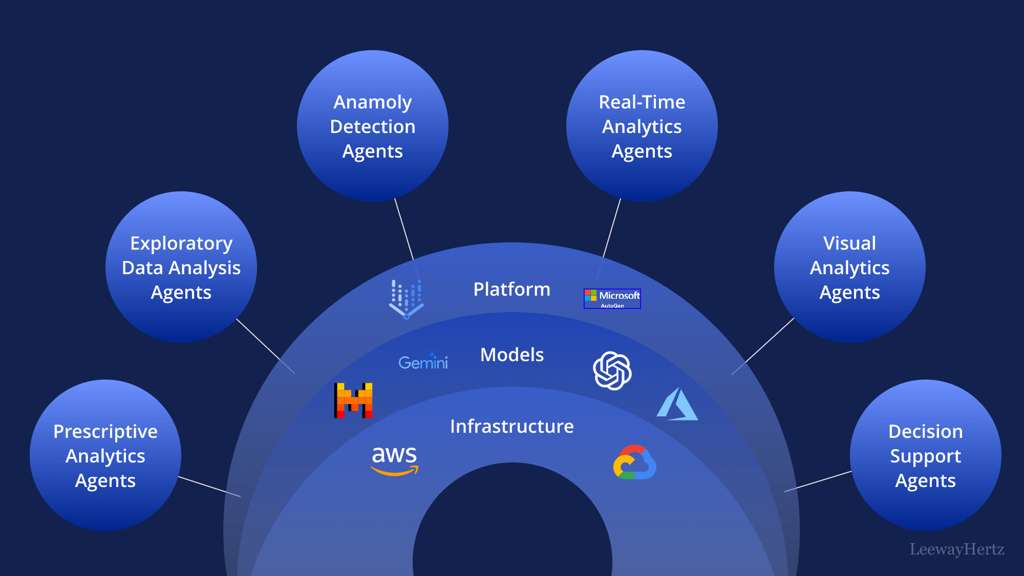

- Neural Networks & Deep Learning (CNN, LSTM): These models represent the cutting edge, capable of modeling highly complex, non-linear patterns.

- Convolutional Neural Networks (CNNs), traditionally used for image analysis, can identify "spatial" patterns in transactional data, making them useful for fraud detection.

- Long Short-Term Memory (LSTM) networks, a type of Recurrent Neural Network (RNN), excel at analyzing time-series data. This makes them invaluable for market risk management (e.g., forecasting volatility) and identifying temporal patterns in operational or systemic risk (ScienceDirect, 2025).

Application Across Key Risk Domains: A Comparative Analysis

The true power of ML is evident when applied across the diverse landscape of financial risks, fundamentally changing the approach in each domain.

Credit Risk: Traditional credit scoring relies on a limited set of historical data points (e.g., FICO scores). In contrast, AI models can analyze thousands of variables in real-time, including transaction history, spending habits, and even alternative data like mobile phone usage or bill payments (DigitalDefynd, 2025). This creates a more dynamic, accurate, and inclusive risk profile, enabling lenders to make better decisions and extend credit to previously underserved populations.

Market Risk: AI moves risk assessment beyond static VaR calculations. By using LSTMs to analyze time-series data and Natural Language Processing (NLP) to gauge sentiment from real-time news feeds and economic reports, institutions can develop predictive forecasts of market volatility and asset price movements. This allows for more agile hedging strategies and proactive portfolio adjustments (Finextra, Sep 2024).

Operational Risk: Instead of relying on periodic manual audits, AI can continuously monitor internal systems to predict operational failures. By analyzing IT logs, transaction processing data, and even external data on supply chain disruptions, AI can issue predictive alerts for potential system outages, process bottlenecks, or compliance breaches before they occur.

Fraud Detection: This is one of AI's most impactful applications. Traditional rule-based systems are rigid and generate a high volume of false positives. AI-powered anomaly detection systems, however, learn the patterns of criminal behavior in real-time. They can analyze thousands of data points per transaction—including location, device, and user behavior—to identify and block fraudulent activity with far greater precision, significantly reducing both financial losses and customer friction (Medium, Mar 2025).

Systemic Risk: Modeling the interconnectedness of the financial system to predict contagion has been a monumental challenge. Advanced techniques like Graph Neural Networks (GNNs) can map and analyze the complex web of relationships between financial institutions, asset classes, and markets. This allows regulators and firms to simulate how shocks might propagate through the system, a task nearly impossible for traditional, siloed methods (Bank of England, Apr 2025).

Real-World Implementation: Case Studies and Proven Impact

The theoretical advantages of AI in risk management are being validated by tangible, real-world applications across the financial sector. Leading institutions are deploying AI-driven solutions to address specific challenges, achieving significant improvements in efficiency, accuracy, and security. The following case studies illustrate the practical impact of this technological shift.

"Each case study reveals how different companies have successfully implemented AI solutions to overcome specific challenges, streamline operations, and deliver exceptional results."

FinSecure Bank: Combating Sophisticated Fraud with Predictive Analytics

- Challenge: The bank was grappling with substantial losses from financial fraud. Its traditional rule-based detection system was inefficient, producing high false positive rates that frustrated customers and failing to adapt to the evolving tactics of fraudsters.

- Solution: FinSecure implemented an advanced AI-driven fraud detection system. This solution used a combination of supervised and unsupervised machine learning models to analyze vast amounts of transaction data in real-time. The system learned from historical fraud cases while also identifying new, anomalous patterns, allowing it to anticipate risk rather than merely react to it.

- Outcome: The implementation led to a remarkable 60% reduction in fraudulent activities within the first year. The significant decrease in false positives also enhanced customer satisfaction and trust (DigitalDefynd, 2025).

QuickLoan Financial: Enhancing Loan Approval with AI

- Challenge: As a growing fintech, QuickLoan Financial struggled with a time-consuming and error-prone manual loan review process. The high volume of applications led to delays, impacting customer satisfaction and operational scalability.

- Solution: The company adopted an AI model that automated the evaluation of loan applications. The system processed both structured data (application forms) and unstructured data (bank statements) using deep learning and NLP. It assessed a wide range of criteria beyond traditional credit scores to generate a more holistic risk profile.

- Outcome: The AI system resulted in a 40% decrease in loan processing time and a 25% improvement in identifying and rejecting high-risk applications. This allowed QuickLoan to scale its operations efficiently while maintaining a low default rate (DigitalDefynd, 2025).

TowneBank: Leveraging AI for Regulatory Compliance and Beyond

- Challenge: TowneBank faced a challenging deadline to comply with the complex Current Expected Credit Loss (CECL) accounting standard, which required analyzing 15 years of historical and forecasting data.

- Solution: The bank turned to an AI-driven framework from SAS to manage the data analysis and complex statistical modeling required for CECL. The system provided a secure and efficient way to access and process data from multiple departments.

- Outcome: TowneBank not only met its compliance deadline but also discovered the framework's broader utility. The bank was able to use the system to answer a range of business questions, from high-level strategic decisions to understanding individual customer needs, effectively turning a regulatory requirement into a strategic asset (VKTR.com, Jul 2024).

Mastercard: Managing Complex Fourth-Party Risk

- Challenge: Mastercard's ecosystem extends beyond its direct partners to a fourth tier of processors and payment facilitators, creating significant risk around data security and compliance that was difficult to monitor.

- Solution: The company deployed an AI-powered platform to manage its third- and fourth-party risk. The system provided comprehensive visibility into these distant entities, categorizing each based on its risk exposure and enabling fast, informed decisions.

- Outcome: The AI solution led to a 66% reduction in the time required to assess third-party risk. It allowed Mastercard to accurately target areas of concern and focus its mitigation efforts, securing its vast and complex payment ecosystem (VKTR.com, Jul 2024).

Navigating the Future: Trends, Challenges, and the Path Forward

As AI becomes more deeply embedded in financial risk management, the industry is at a pivotal juncture. The path forward is paved with both transformative opportunities and significant challenges. Successfully navigating this landscape requires a clear understanding of emerging technologies and a proactive approach to addressing the ethical and regulatory hurdles that accompany them.

Emerging Trends and Technologies

Explainable AI (XAI): The "black box" problem, where the decision-making process of complex models is opaque, is a major barrier to adoption, especially in a highly regulated industry. XAI is emerging as a critical field, developing techniques to make AI models more transparent and interpretable. This is essential not only for meeting regulatory requirements and facilitating model validation but also for building trust among risk managers, executives, and customers who need to understand the "why" behind an AI-generated decision (Nature, Apr 2025).

Generative AI: While much of the focus has been on predictive AI, generative AI is poised to play a significant role. Its applications in risk management include generating highly realistic and complex stress-test scenarios that go beyond historical precedents, creating synthetic data to train models without compromising privacy, and automating the drafting of risk reports and due diligence documentation (Citizens Bank, 2025 Report).

AI Agents: The next frontier is the development of autonomous AI agents. These are systems that can not only monitor risks in real-time but also autonomously execute mitigation strategies and learn from the outcomes. In areas like fraud prevention, an AI agent could instantly block a suspicious transaction and initiate a customer verification process without human intervention. In algorithmic trading, agents could monitor for market manipulation and adjust strategies to mitigate risk (NetSuite, Jun 2025).

Hyper-Personalization of Risk: AI enables a shift from portfolio-level to individual-level risk assessment. By analyzing a customer's unique behavior, AI can facilitate the creation of tailored financial products, dynamic insurance pricing, and personalized investment advice, moving the industry away from one-size-fits-all solutions (Medium, Mar 2025).

Alternative Data Integration: The use of non-traditional data sources will continue to grow. In emerging markets, where formal credit histories are scarce, AI models are using alternative data—such as mobile top-ups, utility payments, and even geolocation patterns—to create financial identities and assess creditworthiness. This not only opens new markets but also promotes financial inclusion (World Economic Forum, Jun 2025).

Overarching Challenges and Ethical Considerations

The integration of AI is not without significant obstacles. Addressing these challenges is paramount to ensuring its responsible and sustainable deployment.

Key Challenges in AI Adoption

- Data Quality and Bias: AI models are only as good as the data they are trained on. Biased data can lead to discriminatory outcomes, perpetuating societal inequalities.

- Regulatory Uncertainty: Regulators are struggling to keep pace with technological change, creating compliance challenges for financial institutions.

- Model Opacity: The "black box" nature of some advanced models makes them difficult to validate, audit, and trust.

- Cybersecurity Risks: AI systems introduce new vulnerabilities that can be exploited by malicious actors.

- Talent and Integration: A significant gap exists in talent with combined expertise in data science, risk management, and ethics. Integrating AI with legacy systems is also a major hurdle.

Data Quality and Bias: The "garbage in, garbage out" principle is a core challenge. If historical training data reflects societal biases (e.g., in lending decisions), AI models will learn and potentially amplify them. Ensuring fairness and mitigating algorithmic bias is a critical ethical and regulatory imperative to prevent discriminatory outcomes (Nature, Apr 2025).

Regulatory Lag and Compliance: Financial regulators face the immense challenge of creating frameworks that can govern a rapidly evolving technology without stifling innovation. Issues like data privacy, model explainability, and cross-border data flows require new, agile regulatory approaches. A 2025 survey by Citizens Bank noted that the perception of legal risks related to AI usage is growing among CFOs (Citizens Bank, 2025 Report).

Model Risk and Opacity: The complexity of deep learning models makes them inherently difficult to interpret. This opacity creates significant model risk, as it is hard to predict how the model will behave under novel market conditions. This lack of transparency is a major concern for auditors and regulators who need to validate model integrity (Bank of England, Apr 2025).

Cybersecurity and New Vulnerabilities: While AI can enhance cybersecurity defenses, it also introduces new attack vectors. Malicious actors can attempt to poison training data, exploit model vulnerabilities, or use AI to develop more sophisticated cyberattacks. The concentration of AI services with a few third-party providers also creates systemic operational risk.

Talent Gap and Organizational Change: The demand for professionals with a hybrid skill set—combining data science, financial risk management, and ethics—far outstrips supply. Furthermore, integrating AI into legacy IT infrastructure and overcoming cultural resistance to change within established workflows are significant organizational hurdles that can slow down adoption.

Conclusion: Towards a More Resilient and Intelligent Financial System

Artificial Intelligence is not a fleeting trend but a structural force that is fundamentally reshaping the foundations of financial risk management. The evidence is clear: AI is moving the industry from a static, reactive discipline, constrained by historical data and manual processes, to a dynamic, proactive, and predictive one. Its capacity to analyze vast and varied datasets, uncover complex non-linear patterns, and operate at unprecedented speed and scale provides a powerful toolkit for navigating the uncertainties of the modern financial landscape.

From the enhanced precision of credit scoring and real-time fraud detection to the predictive power of market volatility forecasting and the holistic view of systemic risk, AI's applications are already delivering substantial value. As technologies like Explainable AI, Generative AI, and autonomous agents mature, their potential to further augment risk management capabilities will only grow.

However, the path to an AI-powered future is not without its perils. The challenges of data bias, regulatory uncertainty, model opacity, and cybersecurity are formidable. Overcoming them requires more than just technological prowess; it demands a deep commitment to responsible governance and ethical principles.

Ultimately, the future of financial risk management is not a binary choice between human and machine. The most effective and resilient model will be a hybrid one, embracing the "human-in-the-loop" imperative. In this paradigm, AI handles the computational heavy lifting—the data processing, pattern recognition, and predictive analysis—while human experts provide the crucial layers of strategic oversight, ethical judgment, and contextual understanding. It is this symbiotic partnership that will unlock the full potential of AI. The institutions that successfully master this balance—fusing technological innovation with responsible governance—will not only mitigate risks more effectively but will also build a more resilient, trustworthy, and intelligent financial future for all.